The Starting Point

Financial planning will mean different things to different people. But everybody benefits from a plan

GOAL SETTING. GOAL GETTING.

It starts with a conversation

FULLY INFORMED

We believe with our help financial planning means you can make fully informed decisions about you, your future and your family.

GOALS BASED

We follow a ‘goals based’ approach which means identifying those ‘need to do’s’ as well as ‘want to do’s’ and setting a strategy to achieve them.

ADAPTIVE

Ultimately, you need to have a plan that is robust enough to meet your demands but flexible enough to adapt when necessary.

our approach

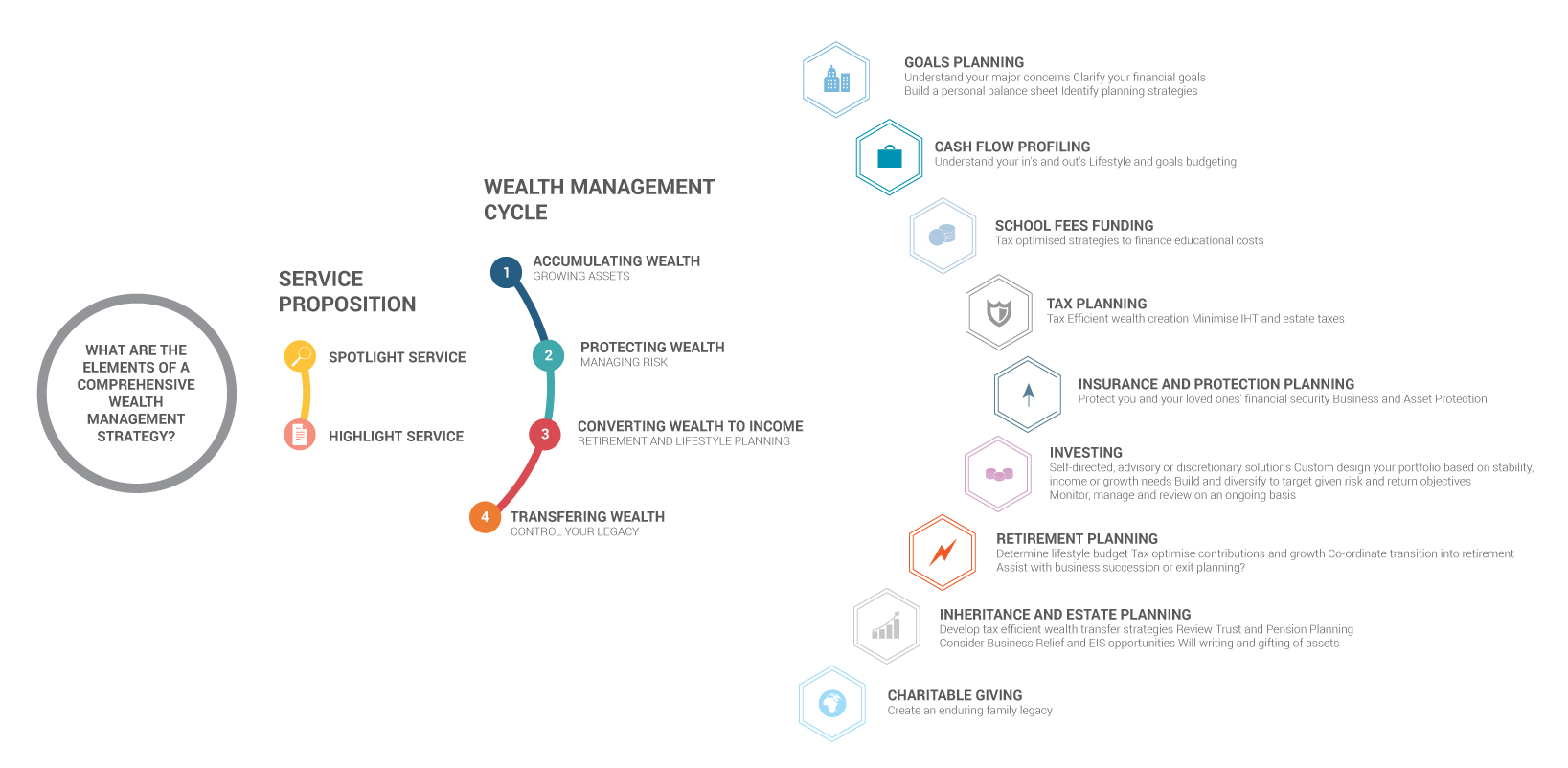

INTRODUCTION TO A GOALS BASED APPROACH

ARIA Private Clients is part of the wider ARIA group, which has a breadth of client including banks, institutions,

pension funds and private clients.

One of the pillars of our proposition is bringing a sense of empowerment to you, a feeling on having control over money matters. Another cornerstone of our approach is to strive to deliver a highly personalised service to each of our clients.

There are different approaches to offering wealth management services, but perhaps the most progressive, is referred to as ‘goals based planning’ Compared to a more traditional approach, goals based planning we believe brings greater clarity to your affairs, and moreover a greater sense of control. Furthermore, it allows us to zero in on what’s really important to you, and identify strategies to reach those very individual goals you may have.

TRADITIONAL FINANCIAL PLANNING vs GOALS BASED PLANNING

|

TRADITIONAL |

GOALS BASED |

|

|

Financial Factors Assets and Liabilities Single'Risk Attitude' | Financial and behavioural factors Client goals What matter's most |

|

Relative to Stock Market: Shorter term focus prevails | Monitoring progress towards established goals |

|

Single Risk tolerance for all investing 'buckets' | Risk capacity against each goal Seeks to calculate confidence levels of reaching a given goal Considers shortfall potential |

|

One overall portfolio | Asset classes or strategies for each individual goal |

GOALS BASED PLANNING IN ACTION: LIFE TRANSITIONS

Ultimately wealth management means: 'money on the move'.

As life transitions, your goals, both pressing needs and ideals, will progress with it. Goals based planning provides an ideal framework to put into place a life cycle wealth management process.

In your 20’s and 30’s

In your 20’s and 30’s

In your 30 to 40’s

In your 30 to 40’s

In your 40’s and 50’s

In your 40’s and 50’s

In your 50’s to 60’s

In your 50’s to 60’s

In your 60’s and 70’s

In your 60’s and 70’s

Mid 70’s and beyond

Mid 70’s and beyond

In your 20's and 30's

We call this ‘foundational planning’ i.e. getting the basics right. We expect that you’ll be focussed on:

-

Funding your lifestyle

-

Getting onto the property ladder

-

Moving on in the world professionally speaking

But the ‘here and now’is more likely to be about:

-

Savings advice

-

Mortgage advice

-

Individual Savings Accounts

-

Learning how to manage your finances

-

Find out more about our ‘Spotlight’

service which could be an ideal fit.

In your 30's and 40's

At this point, there ‘here and now’ could well be:

-

Tie’ing the knot, or putting down roots

-

Aspiring to a larger property

-

Professional development and recognition

-

Perhaps with more disposal income to put to one side

At this point, there ‘here and now’ could well be:

-

Funding education (a professional qualification)

or school fees for children -

Providing for loved ones (income protection, life assurance etc)

-

Pension planning – modifying and managing asset allocations

-

Maximising the tax efficiency of your investments

In your 40's and 50's

At this point, there ‘here and now’ could well be:

-

Teenage children – increasingly more depending

and ready to strike out their own -

Reducing liabilities and paying down the mortgage

-

Aspirational spend may be growing –

more expensive hobbies or goods consumed -

Potentially a dual income household,

with earnings capacity at its maximum

The ‘here and now’ is more likely to be about:

-

Educational costs – this time university fees

-

Optimising your tax liabilities through pension

contributions and ISA portfolios -

Becoming more actuarial in managing assets and

forecasting cash flows and lifetime

budgeting exercises

In your 50's and 60's

At this point, there ‘here and now’ could well be:

-

Children have flown the coup and are no longer

‘financial dependents’, (save for a house deposit!) -

Potential significant equity in property,

resizing or even relocation thoughts -

Disposable income could be peaking

-

Pension and investment consolidation

-

Business planning, be it exit or succession thoughts

The ‘here and now’ could well mean:

-

Estate planning and pre-retirement advice

-

Lifestyle investing – considering market risks and

reducing exposure to riskier asset classes -

Considering and maximising all allowances

-

Retirement options: flexi-working arrangements, early retirement

or a new career!

In your 60's and 70's

At this point, there ‘here and now’ could well be:

-

Taking on new hobbies, maintaining current interests

-

Property investment: a bolthole ‘away from home’

-

Transitioning from gainful employment

to a less ‘structured’ existence -

The next generation

The here and now means a different set of priorities than may have gone before:

-

Inheritance tax planning

-

Gifting to family

-

Optimising your balance sheet to generate an income that

sustains your lifestyle

Mid 70's and beyond

At this point, there ‘here and now’ could well be:

-

Living a healthy and comfortable life will

be high on most people’s agenda. -

Personal health and provision for it

-

Lifestyle considerations including

current living / property arrangements -

Gifting monies to family

There ‘here and now’ means making the most of every day, but more importantly having put into place the arrangements that ensure your legacy is what you would like it to be:

-

Placing assets into Trust

-

Giving assets away to charity

-

Ensuring wills are current

-

Inheritance Tax Planning

-

Ensuring asset allocations are still appropriate for their objectives

-

Care fees funding

HOW DOES IT WORK?

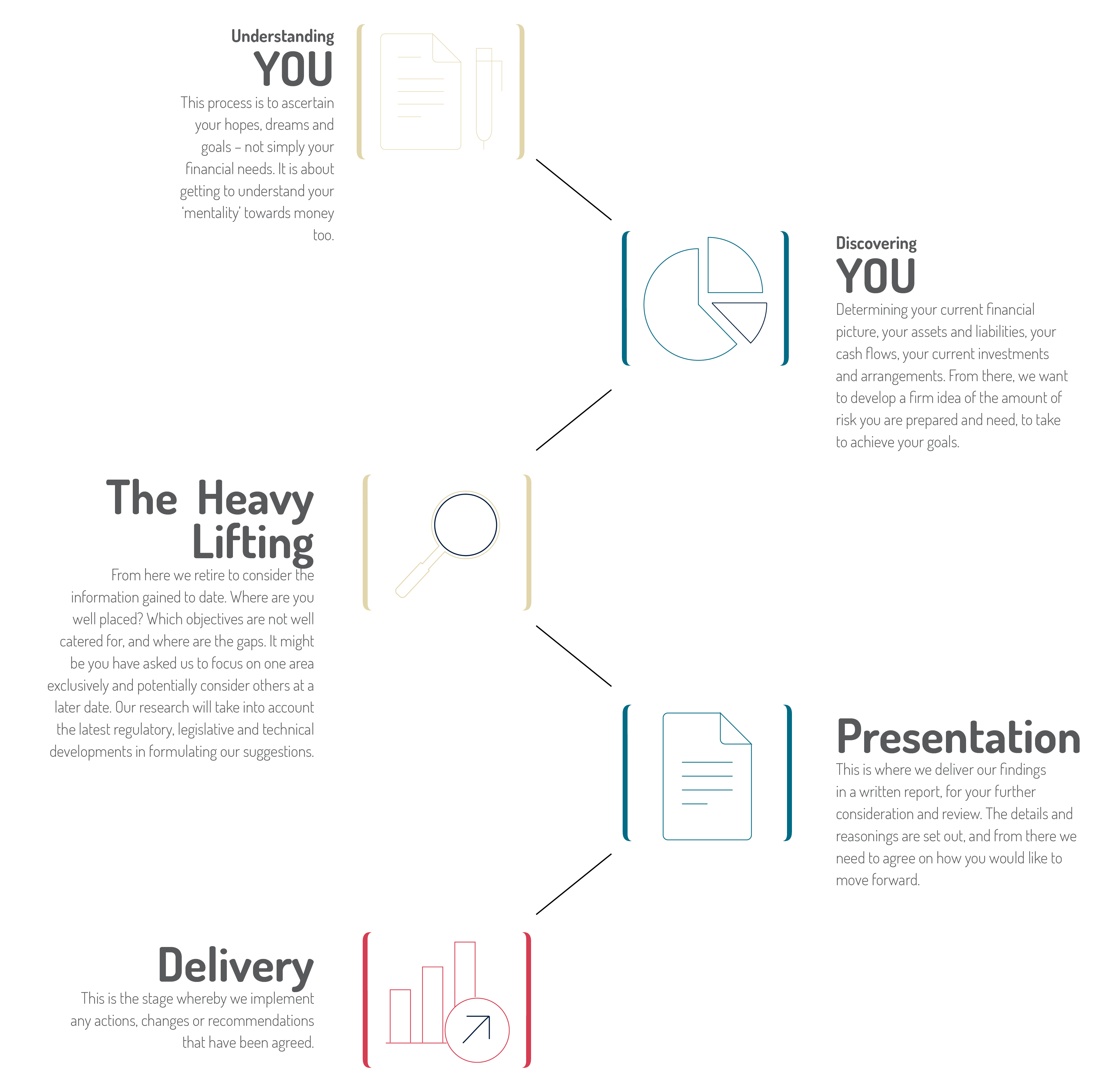

It will always begin with a ‘no obligation’ chat. A free initial meeting to get to know you. Only then can you set out your goals, needs and worries. From there, we’ll set out to identify the best means of addressing them, whilst having an open conversation about the costs involved in doing so.

WHAT WE DO AND WHAT WE ADVISE ON

Solving your problems.

-

Pensions and retirement planning

-

Inheritance tax planning

-

Tax efficient savings

-

Planning for long-term care

-

Wealth protection

-

Life events like divorce or bereavement

- Products and services we can advise on include Investing:

-

'Investment Portfolios

-

Individual Savings Accounts, (ISAs)

-

General Investments Accounts, (GIAs)

-

Investments bonds

- Personal Pension Plans including

-

Stakeholder pensions

-

Self-Invested Personal Pension (SIPPs)

-

QROPs

- Protecting yourself and your family:

(Not currently available in the UK) -

Life and term assurance

-

Income protection

-

Long-term care

- Passing on your Wealth:

-

Will writing

-

Estate Planning and administration

-

Trust creation and management

- Managing your Retirement:

-

Annuities

-

Drawdown Options

-

Taking a lump sum

That’s down to you. It may be a short term engagement in relation to a specific task, or it could be an ongoing relationship borne out of wide ranging financial review. Alternatively, we may simply support your investing needs – be it professionally managing your assets, or providing an advisory or even online stock broking service.

Hopefully the plan that has been prepared is more than sufficient to deliver your goals. However, life being what it is, circumstances will change and at short notice, all of which will need careful consideration and likely adjustments to your financial planning needs along the way. Having an ongoing relationship means that together we will consistently monitor the progress and appropriateness of your arrangements – whilst being on hand to address any changes needed.

There is an abundance of general guidance and information available in the public domain. Be that the moneyadviceservice.org.uk or the Pensions Advisory Service, (pensionsadvisoryservice.org.uk) or information online from newspapers or advice sites. With today's readily available online resources, a lot clearly can be undertaken by oneself.

Technology too we feel should be used wherever possible to liberate, or to empower you. In that respect, we often feel that a mix and match proposition can work well for some, though for others a more self directed service is their preferred route. It may be you feel more comfortable with having a professional adviser consider and set out a personalised approach specific to your circumstances and then take on the responsibility for managing investments, removing another daily distraction. We're very deliberate in offering three different service levels, so should we engage, you will feel that you have just the right level of support.

We would expect to hold a no obligation engagement in the first instance, where there are no fees levied allowing you to feel comfortable to speak openly about your goals without fear of a pending bill. Due to our Spotlight service, we can accommodate those with more simple needs, with readily digestible charging structure that means your investments or needs are well catered for in a very cost effective manner.

The charges typically include an initial fee for providing a well researched and highly relevant set of solutions or arrangements for you in our opinion, to best meet your goals. Those charges mean that we can keep a well resourced team at hand, to keep up to date with the latest regulatory and financial market developments, so that we can keep you well placed at all times.

Please view our Fee Schedule within the Client Agreement for full details

We have sought to offer different service levels for different price points. That being the case, regardless of the complexity of your affairs, we believe we can offer a service that means the value of recommendations, both in terms of the investment returns generated, and the tax that you may save, all contribute towards a very affordable and value for money proposition.

It is not the current value of your asset base that matters – more ensuring it’s longevity to continue to support you throughout your years. Generating sustainable income levels can be difficult in today’s low interest rate environment and therefore having access to specialist research and investment management resource can make all the difference. Moreover, the impact of inflation can be a major threat to the value of income streams and their purchasing power going forwards. As life expectancy generally trends up, considerations such as possible care needs and estate planning will inevitably become planning requirements well after you may have begun your retirement.

We offer both and it will depend on your choice of service level.

Our Highlight service is one whereby we will act as an intermediary between you and a whole market place of products and services. Depending on your level of wealth, we may employ a centralised investment proposition. This is where we have conducted extensive due diligence on a range of providers, including fund managers globally and drawn up a short list of those who provide either best in class or a differentiated proposition, so we can cater to a wide range of preferences and needs. Within the global selection of fund managers, we also offer our own funds, particularly where we feel there isn't a similar proposition available elsewhere.

Spotlight is our focussed advice service and it is limited to certain investment options that we feel are suitable for you, given the information we have to hand. In that respect, it reflects more of a ‘panel’ based approach. In providing solutions to clients we may recommend use of funds managed by us too. We are also likely to implement many of the investment solutions we offer, on our own bespoke wealth management platform. This technology is built on top of SEI Global Investments, one of the world’s largest custodians. To that extent, we do not hold your monies, but are regulated to arrange for custody with third parties

Yes we can. In fact, retirement planning is one of our areas of expertise, and a very common reason to seek out financial advice. However, we do not advise on Defined Benefit pension plans.

Highlight is our comprehensive wealth management proposition which includes both financial planning and investment advice. It often means completing a ‘holistic review’ of your circumstances, before highlighting certain aspects of your financial arrangements for you to consider further. It usually requires an ongoing engagement and within investments north of 50,000 GBP or currency equivalent. We would expect regular contact both through email, telephone and face to face meetings.

related LITERATURE

Call Us

You’re always welcome.

Visit Us

Guildford Business Park,

Guildford, GU2 8XG

United Kingdom